- 第三季度所有事业部及地区的销售业绩均呈现增长(上涨3.6%),前三季度共上涨2.4%。

- 第三季度价格带来2.0%的正面影响,前三季度共带来1.8%的正面影响。

- 第三季度汇率带来2.2%的负面影响,前三季度共带来0.7%的负面影响;第三季度集团架构变动带来0.7%的正面影响,前三季度共带来0.8%的正面影响。

集团董事长兼首席执行官夏朗达对业绩的解析:

“圣戈班2017年前三季度的业绩印证了集团上半年业绩的上升趋势(除去网络攻击的影响)。所有事业部和地区都呈现增长,包括法国。即使价格基准水平更高,我们依然看到其显现出的正面影响,但受到原材料和能源价格上涨的大环境影响,集团所有业务都并非均能如此。集团持续专注其战略重点,自年初至今已签署了23项收购协议,包括最近完成的Glava收购案。

圣戈班已确认2017年的全年目标业绩,我们期待即使在通货膨胀的成本压力下,下半年的同比增长营业额仍然可以超越上半年。“

相比于2016年的293.06亿欧元,2017年前三季度合并后的销售额达305.7亿欧元。

集团架构变动带来的0.8%的正面影响,本质上反映了在亚洲和新兴国家的收购 (Emix, Solcrom, Tumelero)以及在新型小众技术和服务上的收购(H-Old, Isonat, France Pare-Brise)合并后的成果,以及进一步巩固我们在建材分销领域的地位(尤其在北欧国家)的成就。

汇率变动前三季度带来0.7%的负面影响,第三季度带来显著的2.2%的负面影响,主要是由于美元、英镑以及其他一些亚洲和新兴国家货币与欧元之间汇率的下跌。

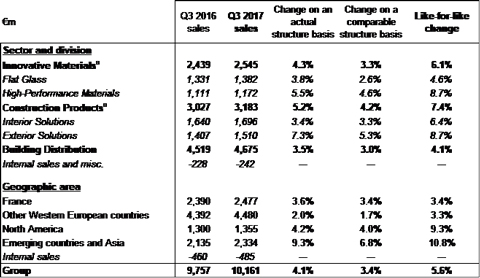

前三季度销售额同比增长4.2%,第三季度达到5.6%,持续了上半年的上升趋势(除却网络攻击的影响)。如7月末网络攻击后集团的声明中所指出的,第二季度集团一些业务部遭受了额外损失,但6月销售额企稳。第三季度业绩上涨3.6%(前三季度上涨2.4%),所有地区和事业部均保持了增长。在能源和原材料成本持续增加的情况下,第三季度价格因素仍带来了2.0%的正面影响(前三季度共1.8%的正面影响)。

a包括业务分部间销售的抵消。

Like-for-like performance of Group Business Sectors

Innovative Materials sales climbed 4.8% over the nine-month period, including 6.1% in the third quarter.

- Flat Glass delivered further good organic growth in the quarter, at 4.6% (5.3% for the nine-month period). The automotive business continued to report good volume growth in all regions, despite a less favorable mix effect compared to the first half. Sales linked to construction markets remained at good levels across Western Europe, with float glass price trends stabilizing and higher prices for transformed glass; Asia and emerging countries again performed well although we expect a negative impact from the earthquake in Mexico which affected our facilities.

- High-Performance Materials (HPM) sales rose 8.7% over the quarter (4.5% over the nine-month period), driven by all regions and businesses, particularly Ceramics which was boosted by exceptionally strong sales of refractories during the summer.

Construction Products (CP) sales moved up 5.0% over the nine-month period and 7.4% in the third quarter.

- Interior Solutions delivered 6.4% organic growth in the quarter (4.8% for the nine-month period), buoyed by healthy volume trends in Western Europe and in Asia and emerging countries. Trading in North America remained stable but with a smaller pricing contribution in a more competitive environment. The price contribution for the division as a whole remained in line with the first half, but still lags behind the rise in raw material and energy costs.

- Exterior Solutions sales rose 8.7% in the third quarter (5.2% over the nine-month period), led by Exterior Products volumes which benefited from a more favorable basis for comparison than in the second quarter and from additional weather-related demand in the US in a competitive price environment. Pipe saw its prices gain ground amid continued strong inflation in raw material costs, while volumes remained affected by the lack of major export contracts. Mortars put in a good quarterly performance in its main regions, despite the Brazilian construction market remaining difficult.

Building Distribution sales rose 3.5% over the nine-month period and 4.1% in the third quarter, in line with first-half trends excluding the impact of the cyber-attack. Trading in France continued to recover, driven by good momentum in new-builds and the first signs of improvement in renovation. Nordic countries as well as the Netherlands and Spain continued to benefit from good market conditions. The UK reported further growth despite an uncertain environment, while Germany was down slightly. A difficult construction market continued to affect Brazil.

Like-for-like analysis by region

- France continued to improve during the quarter, up 3.4% (up 2.6% over the nine-month period), buoyed by dynamic new-build activity. Renovation showed the first signs of improvement in the quarter.

- Other Western European countries delivered further good growth, at 3.3% (2.9% over the nine-month period), led by Nordic countries. The UK reported lower growth driven by prices, with volumes settling and a continued lack of visibility. Germany remained hesitant.

- North America reported 9.3% organic growth over the quarter (4.7% over the nine-month period). Construction volumes continued to trend well, helped by additional weather-related demand; industry was up overall. Pricing slowed amid a tougher basis for comparison and a particularly competitive environment.

- Asia and emerging countries reported further good growth in the third quarter, at 10.8% (8.2% over the nine-month period), driven by all regions.

Strategic priorities and 2017 outlook

The Group continued to focus on its strategic priorities, with 19 acquisitions signed in the nine-month period and 4 finalized in October alone, including Kirson, Megaflex and Glava. The acquisition of the entire share capital of Glava, the insulation market leader in Norway, allows Saint-Gobain to consolidate its positions in Nordic countries.

Pursuant to the agreement between Saint-Gobain and the Burkard family relating to the sale of the shares of Schenker-Winkler Holding (SWH), which holds the majority of Sika voting rights, Saint-Gobain exercised its option to extend the validity of the agreement until June 30, 2018. Saint-Gobain will then have the option to further extend the agreement up until December 31, 2018. This further extension of the sale agreement once again reflects the alignment between the Burkard family and Saint-Gobain and their unwavering determination. The transaction makes strategic, industrial and financial sense for Saint-Gobain and for Sika, for their employees, for their customers and for all of their shareholders. Given the recent appreciation of the euro against the Swiss franc, Saint-Gobain has adapted its acquisition hedging strategy to fix the potential net gain at around €70 million. This is no indication of the future hedging strategy, which will need to evolve in line with market conditions.

The Group expects the following trends for the fourth quarter:

- gradual improvement of construction markets in France;

- continued upbeat trends overall in other Western European countries, despite less visibility in the UK and Germany still hesitant;

- positive market conditions in North American construction;

- good organic growth in Asia and emerging countries;

- ongoing inflationary pressure on costs.

Saint-Gobain confirms its full-year 2017 objective of a like-for-like increase in operating income and expects the like-for-like increase for second-half 2017 to be above the level achieved in first-half 2017 despite ongoing inflationary pressure on costs.

Glossary:

Organic growth and like-for-like changes in sales and operating income reflect the Group’s underlying performance excluding the impact of:

-

changes in Group structure: indicators for the period concerned are calculated based on the scope of consolidation for the previous period (Group structure impact);

-

changes in exchange rates: indicators for the period concerned and those for the previous period are calculated using exchange rates for the previous period (currency impact);

-

changes in applicable accounting policies.

Operating income: see Note 3 to the financial statements in the interim financial report, available by clicking here: https://www.saint-gobain.com/en/finance/regulated-information/half-yearly-financial-report

Free cash flow: cash flow from operations excluding the tax impact of capital gains and losses on disposals, asset write-downs and material non-recurring provisions, less capital expenditure.

Capital expenditure: investments in property, plant and equipment.

Financial calendar

2017 results: February 22, 2018, after close of trading on the Paris Bourse.

|

Analyst/Investor Relations |

Press relations |

||

|

Vivien Dardel Florent Nouveau Floriana Michalowska |

+33 1 47 62 44 29 +33 1 47 62 30 93 +33 1 47 62 35 98 |

Laurence Pernot Susanne Trabitzsch |

+33 1 47 62 30 10 +33 1 47 62 43 25 |

A conference call will be held at 6:30 pm (Paris time) on October 26, 2017: + 33 1 72 72 74 48

Important disclaimer – forward-looking information:

This press release contains forward-looking statements with respect to Saint-Gobain’s financial condition, results, business, strategy, plans and outlook. Forward-looking statements are generally identified by the use of the words “expect”, “anticipate”, “believe", "intend", "estimate", "plan" and similar expressions. Although Saint-Gobain believes that the expectations reflected in such forward-looking statements are based on reasonable assumptions as at the time of publishing this document, investors are cautioned that these statements are not guarantees of its future performance. Actual results may differ materially from the forward-looking statements as a result of a number of known and unknown risks, uncertainties and other factors, many of which are difficult to predict and are generally beyond the control of Saint-Gobain, including but not limited to the risks described in Saint-Gobain’s registration document available on its website (www.saint-gobain.com). Accordingly, readers of this document are cautioned against relying on these forward-looking statements. These forward-looking statements are made as of the date of this document. Saint-Gobain disclaims any intention or obligation to complete, update or revise these forward-looking statements, whether as a result of new information, future events or otherwise raison.

This press release does not constitute any offer to purchase or exchange, nor any solicitation of an offer to sell or exchange securities of Saint-Gobain.

For any further information, please visit www.saint-gobain.com